Why leadership alignment, not technology, is the true driver of AI success.

According to Deloitte’s AI ROI: The Paradox of Rising Investment and Elusive Returns, 85% of organizations increased their AI investment over the past year, and 91% expect to increase spending again. Yet only 6% report realizing satisfactory returns within the first year. Most organizations require two to four years to achieve meaningful ROI, far longer than the seven to twelve months typically expect from major technology investments.

This growing disconnect raises an important question for executive teams and boards alike: if organizations are investing more than ever in artificial intelligence, why are so few realizing meaningful business value?

In my experience, the answer has remarkably little to do with the technology itself. Organizations rarely fail because they selected the wrong large language model, purchased the wrong platform, or lacked technical capability. They struggle because their executive teams never established a shared definition of what AI was expected to accomplish. Without alignment at the top, even the most sophisticated AI initiatives become fragmented, difficult to govern, and nearly impossible to measure. Technology can accelerate transformation, but only leadership alignment determines whether transformation actually occurs.

Leadership Alignment Determines Whether Transformation Actually Occurs

The organizations creating sustainable competitive advantage with AI are not necessarily those making the largest investments. They are the ones aligning strategy, governance, operations, finance, technology, and talent around a common vision of enterprise value before implementation begins.

Across my work advising executive leadership teams, three patterns consistently emerge.

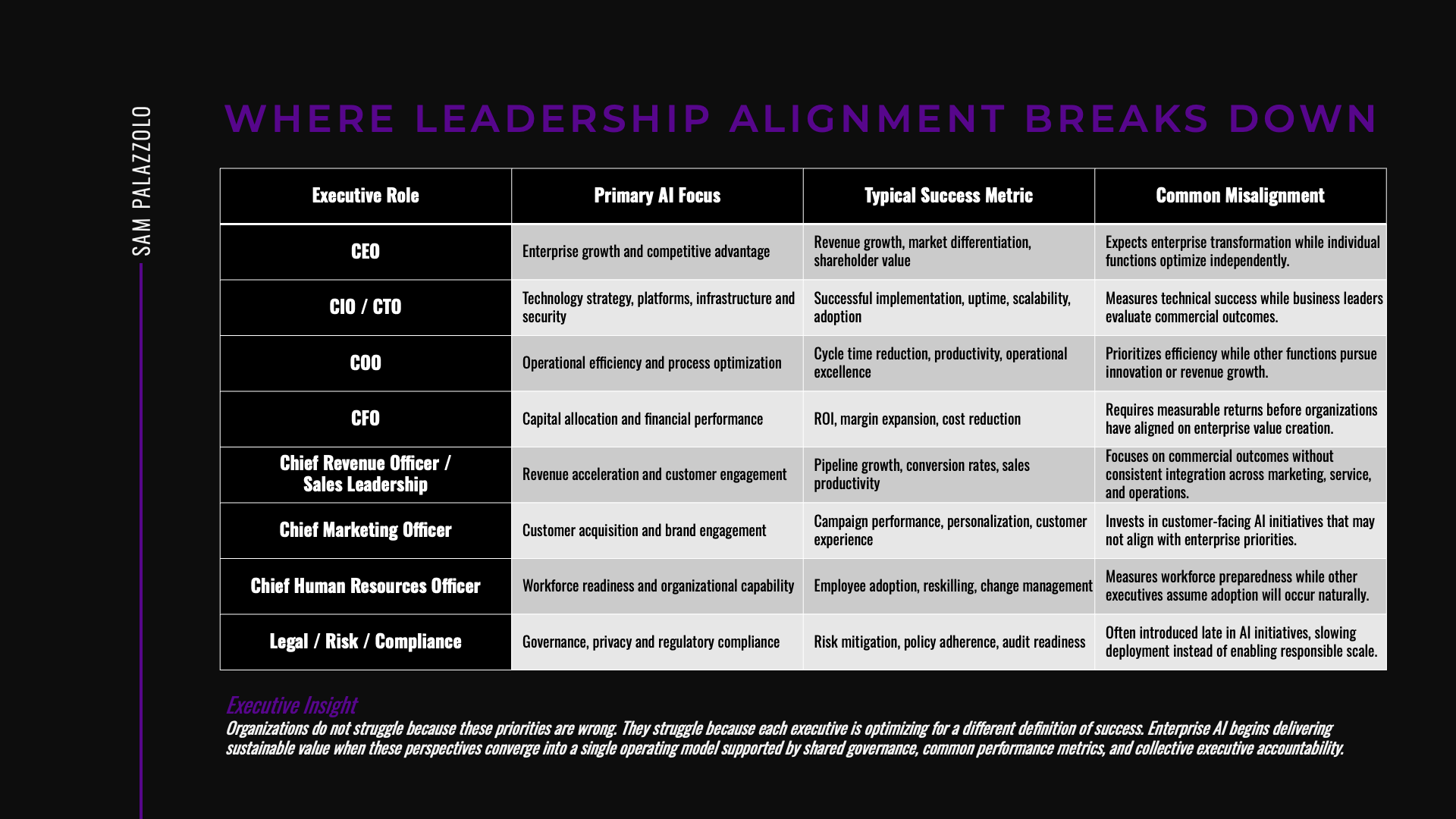

Pattern 1: AI Has No Single Organizational Owner

Artificial intelligence touches every function of the enterprise, yet responsibility for its success typically resides nowhere in particular. Each member of the executive team approaches AI through the lens of individual functional responsibility. The CEO views AI as a catalyst for enterprise growth and competitive positioning. The CIO evaluates platforms, infrastructure, cybersecurity, and technology integration. The COO focuses on operational efficiency and process improvement. The CFO seeks measurable return on investment and disciplined capital allocation. Human Resources evaluates workforce readiness, organizational change, and evolving talent requirements. Legal and Compliance concentrate on governance, privacy, and risk.

Each of these perspectives is rational and necessary in isolation, but collectively insufficient unless integrated into a common enterprise strategy. This is the point at which most organizations lose enterprise coherence without recognizing it. Marketing implements generative AI for content creation. Customer service deploys intelligent chatbots. Finance automates reporting. Operations introduces predictive analytics. Human Resources experiments with AI enabled recruiting and learning platforms. Each initiative delivers incremental value, but few create enterprise value, because the organization has mistaken functional optimization for enterprise transformation.

Rather than building an integrated AI strategy, organizations unintentionally assemble a portfolio of disconnected initiatives. Individual functions optimize locally while the enterprise fails to optimize collectively. The consequence is predictable: different business units establish different priorities, success is measured inconsistently, investments compete rather than reinforce one another, governance becomes fragmented, and accountability becomes unclear. The organization does not lack AI capability. It lacks enterprise leadership.

“AI does not fail because organizations lack technology. It fails because leadership lacks alignment on what success actually looks like.”

Sam Palazzolo

Pattern 2: Leaders Agree on AI’s Potential but Define Success Differently

Few executive teams question whether artificial intelligence will reshape their industry. The disagreement begins when leaders attempt to define what success actually looks like. For one executive, success means reducing operating costs. For another, it means accelerating innovation. Sales leadership prioritizes revenue growth and customer engagement. Finance emphasizes productivity improvements and margin expansion. Operations focuses on cycle times and efficiency. Human Resources measures adoption, capability development, and employee effectiveness. Each objective is legitimate on its own terms, but none is comprehensive.

When every executive measures AI through a different scorecard, organizational alignment deteriorates long before implementation begins. Resources become fragmented, priorities shift, teams receive inconsistent direction, and performance metrics become increasingly difficult to reconcile. The organization remains committed to AI investment; it simply lacks a common operating definition of success.

The most successful AI transformations begin long before selecting vendors, deploying copilots, or launching pilots. They begin with executive agreement on the business outcomes AI is expected to deliver and the enterprise metrics that will define success. Only then does technology become an accelerator rather than a distraction.

“Every executive has a valid perspective on AI. The competitive advantage comes when those perspectives become one enterprise strategy.”

Sam Palazzolo

Pattern 3: AI Investment Is Accelerating Faster Than Organizational Readiness

The pace of AI investment continues to accelerate. Enterprise software providers are embedding AI into nearly every application. Organizations are expanding licenses, funding pilots, and launching new use cases at unprecedented speed. Boards increasingly expect management teams to articulate credible AI strategies capable of improving both competitiveness and enterprise performance.

Leadership readiness has not advanced at the same pace. Many organizations have invested heavily in AI technologies while investing comparatively little in governance, executive accountability, operating models, workforce enablement, or change management. Technology adoption has outpaced organizational maturity, and this imbalance creates an increasingly familiar pattern: executives expect transformational outcomes from organizations that have not yet established the leadership disciplines necessary to sustain transformation.

Technology scales rapidly. Alignment does not. Alignment requires deliberate communication, shared accountability, executive sponsorship, clear governance, and consistent decision-making. Organizations that overlook these fundamentals frequently mistake implementation for transformation, and the two are fundamentally different. Implementation introduces technology. Transformation changes how the enterprise creates value.

“Technology scales in months. Leadership alignment often takes years. The organizations that close that gap first will define the next decade.”

Sam Palazzolo

Executive Imperative: Leadership Alignment Is the Competitive Advantage

Artificial intelligence is no longer simply a technology initiative. It is an enterprise leadership challenge. Organizations that create lasting competitive advantage through AI will not necessarily be those with the largest technology budgets, the most sophisticated models, or the greatest number of pilots. They will be the organizations whose executive teams align strategy, governance, operations, finance, technology, and talent around a common vision of enterprise value.

Leadership alignment transforms AI from a collection of disconnected initiatives into an integrated business capability. It establishes ownership, creates accountability, aligns investment priorities, and enables consistent decision-making. Most importantly, it provides the organizational discipline required to convert technological capability into measurable business performance.

Artificial intelligence is rapidly becoming a strategic differentiator. Leadership alignment will determine which organizations capitalize on that opportunity and which continue searching for returns that remain just out of reach.

“Artificial intelligence is no longer a technology initiative. It is the executive operating model that will separate tomorrow’s market leaders from everyone else.”

Sam Palazzolo

The question facing executive teams is no longer whether to invest in artificial intelligence. Most already have. The more consequential question is whether the leadership team shares a common understanding of why those investments are being made, how success will be measured, and who will ultimately be accountable for delivering enterprise value. Until those questions are answered collectively, AI performance will continue to fall short of its potential. Technology can accelerate execution, but only aligned leadership can accelerate enterprise transformation.

Questions Every Executive Team Should Be Asking

As artificial intelligence becomes embedded across every function of the enterprise, executive teams should routinely ask themselves five questions:

- Do we have a shared definition of AI success across the executive team?

- Who owns enterprise AI outcomes beyond individual functional initiatives?

- Are we measuring business value or simply tracking technology adoption?

- Does our governance model enable responsible, scalable, enterprise-wide decision-making?

- Are we scaling AI capabilities faster than we are developing leadership alignment and organizational readiness?

Organizations that can answer these questions with confidence are far more likely to translate AI investment into sustainable competitive advantage. Those that cannot may discover that their greatest obstacle is not the technology they purchased. It is the leadership alignment they never established.

Sam Palazzolo

Operator. Investor. Educator. Enterprise Value Strategist.

Scaling organizations. Maximizing enterprise value.